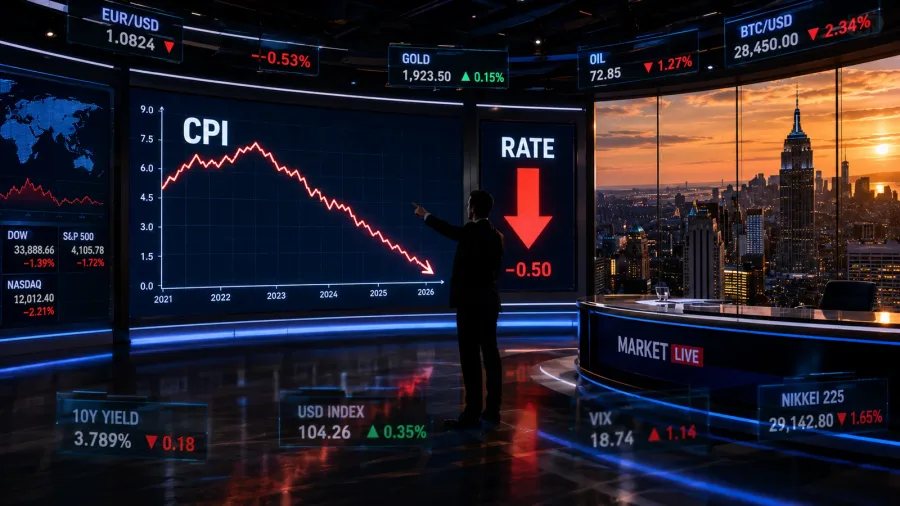

The U.S. Bureau of Labor Statistics delivered a jolt to global financial markets on the morning of July 17, 2026, by reporting that the Consumer Price Index for June had cooled far more than anticipated. The annual headline inflation rate fell to 2.4%, a significant undershoot of the 2.7% consensus forecast and the lowest reading in a year and a half. This data point immediately rewired expectations for the Federal Reserve's monetary policy path, triggering a powerful rally in equities and a sharp drop in both bond yields and the U.S. dollar.

A seismic shift across asset classes: Equities surge as dollar tumbles

The initial market reaction was swift and decisive, reflecting a classic 'risk-on' pivot. The S&P 500 index jumped 1.8% in early trading, while the tech-heavy Nasdaq Composite outpaced it with a 2.5% surge. The rally was broad-based, but the most dramatic moves were seen in rate-sensitive sectors. Real estate investment trusts (REITs) and high-growth technology companies, whose future cash flows are discounted at lower rates, led the charge. This bullish sentiment was fueled by the growing conviction that the Federal Reserve's aggressive tightening cycle, which had kept the benchmark interest rate at a restrictive 5.50% throughout the first half of 2026, was finally over.

Treasury yields plunge and the dollar index hits a 14-month low

In a stark reversal of the 'higher-for-longer' narrative that had dominated markets, the yield on the benchmark 10-year U.S. Treasury note plummeted by more than 15 basis points to 3.65%. This massive rally in bond prices signaled a fundamental reassessment of the economic outlook. Simultaneously, the U.S. Dollar Index (DXY), which measures the greenback against a basket of major currencies, broke below the 102 level, flirting with its lowest point in 14 months. The euro surged past the 1.12 handle against the dollar, while the Japanese yen strengthened to around 138 per dollar. This currency turmoil underscored a rapid unwinding of long-dollar positions by global macro hedge funds.

Decoding the Fed's next move: Is a September rate cut now a certainty?

This inflation report is the most consequential piece of data the Federal Open Market Committee (FOMC) will receive before its highly anticipated September 18, 2026, meeting. Fed Chair Jerome Powell had consistently emphasized the need for 'greater confidence' that inflation was on a sustainable path to the 2% target before easing policy. The June core CPI figure, which excludes volatile food and energy prices, provided exactly that. It decelerated to 2.6% year-over-year from 2.9%, driven largely by a long-awaited moderation in shelter costs, a component that had proven stubbornly high throughout 2025 and early 2026.

Wall Street economists weigh in with cautious optimism

Leading financial institutions were quick to revise their forecasts. Goldman Sachs' chief U.S. economist stated in a client note that 'this report was the missing piece of the puzzle, making a 25-basis-point cut in September a near certainty.' However, dissenting voices from more hawkish circles warned against over-interpreting a single data point, pointing to the still-elevated services inflation and potential base effects from energy prices. Nevertheless, the CME FedWatch Tool, a barometer of market sentiment, showed traders assigning an 85% probability to a rate cut at the September meeting, a dramatic jump from the 60% chance priced in just a day earlier. The debate has now shifted from whether the Fed will cut to how deep the cutting cycle will be.

A green light for emerging markets: Capital flows shift as the dollar weakens

The prospect of a more dovish Federal Reserve acted as a powerful catalyst for emerging market assets. A weaker dollar and lower U.S. Treasury yields reduce the attractiveness of American assets, pushing global investors to search for higher returns in riskier corners of the world. The MSCI Emerging Markets Index rallied over 2% on the day, with currencies like the South African Rand and the Brazilian Real posting significant gains against the greenback. This environment of abundant global liquidity and a softening dollar is historically a boon for developing economies, lowering their external borrowing costs and easing financial conditions.

How frontier and developing economies can capitalize on the Fed pivot

For countries with high external financing needs, such as Turkey, the shift in the global monetary tide offers a crucial window of opportunity. A sustained decline in the U.S. dollar and global interest rates could significantly reduce the cost of rolling over foreign debt and attract portfolio inflows into local equity and bond markets. International credit rating agencies have noted that this external backdrop, combined with continued orthodox domestic policies, is a positive development. The key for these economies will be to use this breathing room to rebuild foreign exchange reserves and anchor domestic inflation expectations, rather than simply enjoying a temporary liquidity-driven rally in local asset prices.

Portfolio playbook for the second half of 2026: From cash to real assets

The dramatic shift in the macroeconomic landscape is forcing a wholesale recalibration of investment strategies. The 'TINA' (There Is No Alternative) era, which had driven investors into a narrow set of mega-cap tech stocks, is facing its sternest test. With the yield on cash and short-term bills set to decline, a massive pool of sidelined capital is beginning to move into longer-duration bonds and dividend-paying equities. The price of gold, a classic hedge against dollar weakness and lower real rates, vaulted back above the $2,500 per ounce mark, signaling that demand for hard assets remains robust. The new playbook emphasizes diversification, moving away from an over-concentration in U.S. large-cap growth and toward a more balanced mix of value, international, and real asset exposures.

The great rotation: Small-caps and cyclical stocks take the lead

One of the most telling signs of the new market regime was the performance of the Russell 2000 index, which tracks small-capitalization companies. It surged over 3.5%, dramatically outperforming the tech giants that had led the market for the previous two years. This suggests a profound sector rotation is underway, with capital flowing from overvalued, AI-driven technology names into cyclical and rate-sensitive sectors. Sectors such as homebuilding, automotive, and renewable energy, which are highly dependent on financing costs, are poised to be the primary beneficiaries. For investors, this transition provides a compelling opportunity to rebalance portfolios away from a purely growth-oriented strategy and towards a more value-conscious approach focused on tangible cash flows and dividends.